The 2026 Multifamily Housing Crisis: Why Landlords Are Struggling to Fill Units in the Sun Belt and Midwest

Last updated: February 25, 2026

Key Takeaways

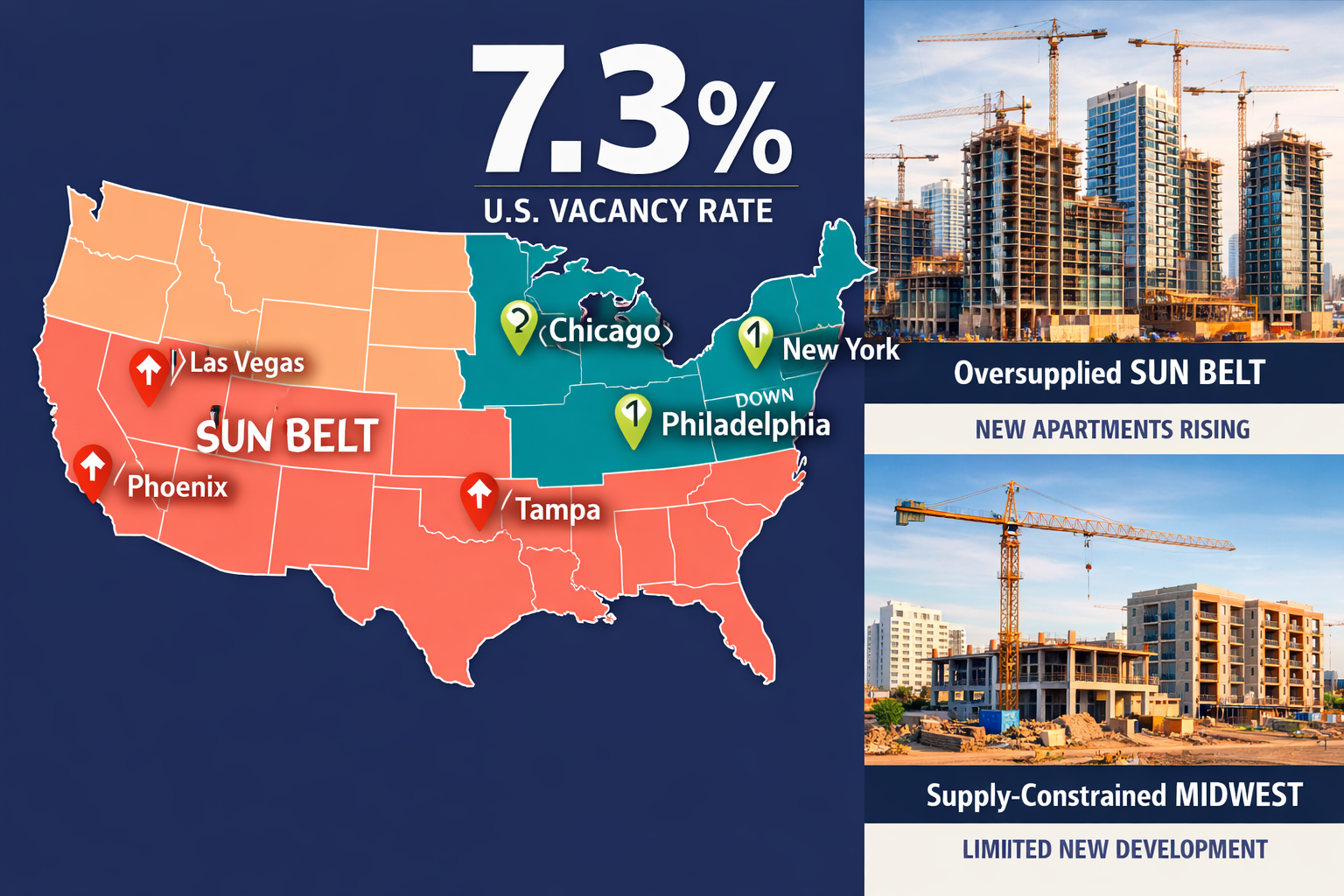

- Record vacancy rates reached 7.3% nationally in January 2026, the highest level since at least 2017, as massive supply collides with weakening demand[4][3]

- Rent growth turned negative at -1.4% year-over-year, with effective rents down 0.8% during 2025 despite remaining 25% above 2019 levels[1][4]

- Leasing timelines extended to an average of 41 days, while over 35% of properties now offer concessions to attract tenants[4]

- Sun Belt markets struggle most with oversupply, particularly Phoenix, Tampa, and Las Vegas, where aggressive construction outpaced absorption[3]

- Midwest markets show resilience with supply-constrained metros like Chicago, New York, and Philadelphia experiencing stronger rent growth[3]

- Property values declined 4% in 2025 and remain roughly 28% below the 2022 peak, though still 8% above 2019 levels[3]

- Construction pipeline moderating with multifamily starts expected to fall 5% in 2026 to 392,000 units annually[2][3]

- Landlords face operational pressure from extended vacancy periods, rising concession costs, and compressed net operating income

Quick Answer

The 2026 multifamily housing crisis stems from a historic supply glut colliding with softening demand. Over 600,000 units delivered in 2024 and 500,000 in 2025 flooded markets—particularly in the Sun Belt—faster than renters could absorb them[4]. Vacancy rates hit 7.3% nationally, forcing landlords to extend leasing timelines to 41 days and offer concessions at over 35% of properties[4]. Meanwhile, rent growth turned negative at -1.4%, squeezing property owners who face higher operating costs and debt service on recently completed buildings[1][4].

What Is Causing the 2026 Multifamily Housing Crisis?

The 2026 multifamily housing crisis results from an unprecedented construction boom that delivered far more units than the market could absorb, combined with slowing population growth and changing renter preferences.

Between 2024 and 2025, developers added over 1.1 million new multifamily units to the national housing stock—well above historical absorption rates[4]. This massive supply influx was planned during the pandemic-era rental surge when demand seemed insatiable and rents climbed rapidly. However, by the time these projects reached completion, market conditions had shifted dramatically.

Key contributing factors include:

- Development pipeline lag – Projects started in 2022-2023 when financing was easier and rent growth projections were optimistic

- Slowing population growth – Demographic trends shifted, reducing the pool of potential renters in key markets[5]

- Elevated construction costs – Tighter financing and higher building expenses created pressure on new developments[3]

- Regional oversupply – Sun Belt markets that experienced explosive pandemic-era growth saw the most aggressive construction activity

- Economic uncertainty – Potential renters delayed household formation or chose alternative housing options

The result is a fundamental supply-demand imbalance. Markets built for yesterday's growth projections now face today's softer demand reality.

Why Are Sun Belt Markets Experiencing the Worst Vacancy Rates?

Sun Belt markets face the most severe challenges in the 2026 multifamily housing crisis because developers concentrated construction activity in these fast-growing regions, creating localized oversupply that overwhelmed absorption capacity.

Cities like Phoenix, Tampa, and Las Vegas experienced particularly weakened rent performance in 2025 as new supply flooded these markets[3]. These metros attracted massive development investment based on pandemic-era migration patterns when remote workers and retirees relocated from expensive coastal cities seeking affordability and lifestyle benefits.

Why Sun Belt markets are struggling:

| Challenge | Impact |

|---|---|

| Concentrated development | Multiple large projects delivered simultaneously in the same submarkets |

| Slowing migration | Return-to-office mandates reduced remote worker relocations |

| Speculative building | Developers chased past growth trends rather than future demand |

| Limited barriers to entry | Available land and favorable zoning enabled rapid construction |

| Competition intensity | Similar properties targeting identical renter demographics |

Phoenix exemplifies this dynamic. The metro added thousands of units targeting the same price-conscious renter segment, creating fierce competition. Landlords responded with aggressive concession packages—free rent, waived fees, upgraded amenities—that eroded effective rental income even as asking rents remained elevated.

Common mistake: Property owners assumed Sun Belt growth would continue indefinitely and failed to model downside scenarios where supply exceeded demand.

How Are Midwest Markets Performing Differently in the Crisis?

Midwest markets are demonstrating relative strength during the 2026 multifamily housing crisis because supply-constrained conditions in metros like Chicago, New York, and Philadelphia created healthier demand-supply balances.

Unlike Sun Belt markets, many Midwest and Northeast metros experienced limited new construction due to higher land costs, stricter zoning regulations, and more complex development approval processes. This supply constraint protected existing landlords from the oversupply pressures plaguing other regions[3].

Midwest market advantages:

- Supply discipline – Development barriers prevented speculative overbuilding

- Stable demand – Established employment bases provided consistent renter pools

- Less volatility – Markets avoided both the pandemic surge and subsequent correction

- Investment activity – Multifamily sales in Midwest metros showed particularly strong growth in 2025[3]

- Rent stability – Moderate but positive rent growth rather than dramatic swings

Choose Midwest markets if you prioritize stability over explosive growth potential. These metros offer lower vacancy risk but also more modest upside during expansion periods.

The performance gap highlights a fundamental real estate principle: supply constraints create value. Markets where development faces natural or regulatory barriers maintain better occupancy rates and pricing power during downturns.

What Operational Challenges Face Landlords with High Vacancy Rates?

Landlords struggling with high vacancy rates in the 2026 multifamily housing crisis face compressed net operating income, extended marketing costs, and difficult decisions about pricing versus occupancy trade-offs.

The average 41-day list-to-lease timeline represents a significant operational burden[4]. Each additional week a unit sits vacant means lost rental income that can never be recovered, plus ongoing expenses for utilities, maintenance, and marketing that continue regardless of occupancy.

Critical operational challenges:

- Revenue compression – Negative rent growth of -1.4% combined with concession costs reduces effective rental income[1][4]

- Marketing expense escalation – Longer lease-up periods require sustained advertising, broker fees, and leasing staff overtime

- Concession strategy dilemmas – Deciding between upfront rent discounts versus ongoing amenity upgrades

- Maintenance during vacancy – Keeping units show-ready while minimizing utility and upkeep costs

- Staff morale impact – Leasing teams face pressure when conversion rates decline despite increased effort

- Debt service coverage – Properties with recent financing face covenant pressure when NOI drops

- Capital expenditure timing – Determining whether to invest in upgrades or preserve cash during uncertainty

Decision rule: If your property's debt service coverage ratio drops below 1.25x, prioritize occupancy over asking rent. A unit leased at 5% below market generates more cash flow than an empty unit at "market" rates.

Edge case: Properties that completed construction in late 2024 or early 2025 face the most acute pressure because they carry peak construction costs, higher interest rates on recent financing, and must compete against both existing stabilized properties and newer competitors offering aggressive lease-up concessions.

What Strategies Help Landlords Fill Units in Oversupplied Markets?

Landlords can improve occupancy in oversupplied markets by implementing targeted retention programs, right-sizing concession strategies, and differentiating their properties through amenities and service quality rather than price alone.

Effective tenant retention strategies:

- Renewal incentives – Offer existing tenants modest rent increases (0-2%) rather than market adjustments to avoid turnover costs

- Lease extension bonuses – Provide small concessions (free parking month, upgraded appliance) for early renewal commitments

- Community building – Host resident events that create social connections and reduce move-out likelihood

- Responsive maintenance – Fast service request resolution builds goodwill and retention

- Flexible lease terms – Offer 6, 9, or 15-month options to capture renters with non-standard timelines

Smart concession approaches:

Choose short-term concessions (first month free) over permanent rent reductions when possible. This preserves your rent roll for future refinancing or sale valuations. A property with $1,500/month asking rents and one month free ($1,375 effective) appears stronger to lenders than one with $1,375 asking rents.

Differentiation tactics:

- Technology integration – Smart home features, package lockers, and mobile apps appeal to tech-savvy renters

- Niche targeting – Focus on specific demographics (pet owners, remote workers, students) with tailored amenities

- Service excellence – Train staff to provide hospitality-level service that justifies premium positioning

- Sustainability features – Energy-efficient appliances and utilities can reduce renter costs even at higher base rents

Common mistake: Matching every competitor's concession package creates a race to the bottom. Instead, identify your property's unique strengths and market to renters who value those specific attributes.

How Will the Multifamily Market Evolve Through 2026 and Beyond?

The multifamily market will gradually stabilize through 2026 as construction activity moderates and existing supply gets absorbed, though recovery timelines vary significantly by region and property class.

Multifamily starts are anticipated to fall 5% in 2026 to 392,000 units annually and decline an additional 6% in 2027 to 367,000 units[2][3]. This construction pullback stems from tighter financing conditions and elevated building costs that make new projects economically challenging[3].

Expected market evolution:

2026 outlook:

- Vacancy rates peak in Q2-Q3 before beginning gradual decline

- Rent growth remains negative or flat in oversupplied Sun Belt markets

- Supply-constrained markets see modest positive rent growth (1-3%)

- Property sales volume continues recovering as pricing stabilizes

- Distress opportunities emerge for well-capitalized buyers

2027-2028 projections:

- Reduced deliveries allow demand to catch up with supply

- Vacancy rates normalize toward 5-6% nationally

- Rent growth returns to low single digits (2-4%) in most markets

- Development activity remains subdued due to cautious lending

- Property values stabilize and begin modest appreciation

Choose this strategy if:

- You have strong reserves – Properties that can weather 12-18 months of compressed income will benefit when markets tighten

- You focus on Class A locations – Prime locations in supply-constrained markets recover fastest

- You prioritize operational excellence – Well-managed properties gain market share during downturns

Avoid these markets if you need immediate cash flow: Sun Belt metros with 18+ months of additional supply pipeline will face extended pressure before recovery begins.

What Does Property Value Decline Mean for Multifamily Investors?

Property value declines create both challenges for current owners and opportunities for new investors, with multifamily assets falling 4% in 2025 and sitting roughly 28% below 2022 peak values[3].

For existing owners, the value decline impacts refinancing options, equity positions, and exit strategies. Properties purchased or refinanced at 2022 peak values may face loan-to-value covenant issues or require additional equity injections when debt matures.

For prospective buyers, the correction creates entry opportunities at more reasonable valuations. Properties trading 28% below peak prices offer better cash-on-cash returns and reduced downside risk, particularly in markets where fundamentals remain solid despite temporary oversupply.

Investor considerations:

| Scenario | Action |

|---|---|

| Maturing debt in 2026-2027 | Negotiate extensions or prepare equity injection; avoid forced sales |

| Strong cash reserves | Consider acquiring distressed assets in supply-constrained markets |

| Floating rate exposure | Explore rate cap extensions or fixed-rate conversion options |

| Value-add properties | Delay major renovations until market conditions improve |

| New acquisitions | Underwrite conservative rent growth (0-2%) for next 24 months |

Important context: While values declined 28% from peak, they remain 8% above 2019 levels[3]. This suggests the 2022 peak represented overvaluation rather than the current market reflecting fundamental distress.

Dallas continued leading the nation in apartment investment volume at $9.6 billion in 2025, up 3.0% from the prior year, with cap rates averaging 5.5%[1]. This sustained transaction activity indicates investor confidence in long-term fundamentals despite near-term headwinds.

Frequently Asked Questions

How long will the 2026 multifamily housing crisis last?

The crisis will likely persist through mid-to-late 2026 as existing supply gets absorbed, with recovery beginning in 2027 as construction activity moderates to 392,000 units annually and demand catches up with supply[2][3]. Sun Belt markets may require 18-24 months for full recovery.

Should landlords lower rents or offer concessions?

Offer short-term concessions (one month free, waived fees) rather than permanent rent reductions. Concessions preserve your rent roll for property valuations and future refinancing while still providing immediate move-in value to prospective tenants.

Which markets offer the best investment opportunities in 2026?

Supply-constrained Midwest and Northeast markets like Chicago, New York, and Philadelphia offer better near-term stability, while distressed Sun Belt properties may provide long-term value for investors with patient capital and strong reserves[3].

What vacancy rate is considered healthy for multifamily properties?

A healthy vacancy rate typically ranges from 5-6% nationally. The current 7.3% rate indicates oversupply, though individual property performance varies based on location, property class, and management quality[4][3].

How are property sales performing during the crisis?

Multifamily property sales rebounded 15% in 2025 after a three-year slump, with 80% of metros seeing increased sales activity, indicating investor confidence despite operational challenges[3].

What concession rate is normal in multifamily housing?

Concession rates typically run 10-15% in balanced markets. The current 35%+ rate indicates significant landlord pressure to fill units and suggests oversupply conditions[4].

Will rent prices drop significantly in 2026?

Rents already declined 1.4% year-over-year nationally, with effective rents down 0.8% during 2025[1][4]. Further declines are possible in oversupplied Sun Belt markets, while supply-constrained metros may see flat to modest positive growth.

How does the 2026 crisis compare to previous multifamily downturns?

The 2026 crisis is primarily supply-driven rather than demand-driven, unlike the 2008-2009 recession. Fundamentals remain relatively healthy with strong employment, but excessive construction created temporary imbalances.

What is driving the construction slowdown in 2026?

Tighter financing conditions and elevated construction costs are reducing new starts, with multifamily construction expected to fall 5% in 2026 and another 6% in 2027[2][3].

Should property owners invest in upgrades during high vacancy periods?

Focus on high-ROI improvements that differentiate your property (smart home tech, package systems, pet amenities) rather than major capital expenditures. Preserve cash for operations until markets stabilize.

How can landlords improve tenant retention rates?

Offer existing tenants minimal rent increases (0-2%), provide renewal bonuses, respond quickly to maintenance requests, and build community through resident events. Retention costs far less than turnover and re-leasing.

What cap rates are investors targeting in 2026?

Cap rates vary by market but averaged 5.5% in high-volume markets like Dallas[1]. Investors are targeting higher cap rates (6-7%+) in oversupplied Sun Belt markets to compensate for near-term operational risk.

Conclusion

The 2026 multifamily housing crisis presents significant operational challenges for landlords, particularly in oversupplied Sun Belt markets where vacancy rates reached 7.3% and rent growth turned negative[4][3]. However, this crisis is temporary and supply-driven rather than a fundamental breakdown in rental demand.

Actionable next steps for property owners:

- Prioritize retention – Lock in existing tenants with modest increases rather than facing 41-day re-leasing timelines[4]

- Right-size concessions – Use strategic, short-term incentives rather than permanent rent reductions

- Monitor cash reserves – Ensure 6-12 months of operating reserves to weather extended vacancy periods

- Differentiate your property – Invest in amenities and service that justify your positioning versus competitors

- Prepare for refinancing – Properties with maturing debt should begin lender conversations early

- Evaluate distressed opportunities – Well-capitalized investors should explore acquisition opportunities in supply-constrained markets

The construction pipeline is already moderating, with starts expected to fall 5% in 2026 and another 6% in 2027[2][3]. As new supply decreases and existing inventory gets absorbed, markets will gradually rebalance. Properties that maintain strong operations and preserve tenant relationships through this challenging period will emerge well-positioned for the next growth cycle.

For investors and landlords, the key is recognizing that oversupply is temporary but operational decisions have lasting consequences. Focus on sustainable occupancy strategies rather than short-term fixes that compromise long-term property value.

References

[1] U S Multifamily Market Snapshot February 2026 - https://arbor.com/blog/u-s-multifamily-market-snapshot-february-2026/

[2] 2026 Housing Outlook Ongoing Challenges Cautious Optimism And Incremental Gains - https://www.nahb.org/news-and-economics/press-releases/2026/02/2026-housing-outlook-ongoing-challenges-cautious-optimism-and-incremental-gains

[3] Multifamily Market Expected To Cool In 2026 As Vacancies Rise - https://www.nahb.org/news-and-economics/press-releases/2026/02/multifamily-market-expected-to-cool-in-2026-as-vacancies-rise

[4] Navigating Rental Landscape Feb 2026 - https://www.apartmentlist.com/rental-management/navigating-rental-landscape-feb-2026

[5] Single Family Multifamily Construction Bring On The Supply Just As Population Growth Slows To A Crawl - https://wolfstreet.com/2026/02/18/single-family-multifamily-construction-bring-on-the-supply-just-as-population-growth-slows-to-a-crawl/