The Senior Housing Boom: Investment Opportunities as Baby Boomers Turn 80

The Senior Housing Boom 2026: Investment Opportunities as Baby Boomers Turn 80 represents one of the most significant demographic shifts in modern history, creating unprecedented demand for wellness-focused, technology-enabled senior living communities.

Last updated: February 3, 2026

The Senior Housing Boom 2026: Investment Opportunities as Baby Boomers Turn 80 represents one of the most significant demographic shifts in modern history, creating unprecedented demand for wellness-focused, technology-enabled senior living communities. As approximately 11,000 Baby Boomers turn 80 every day in 2026, investors face a rare opportunity to capitalize on surging demand amid critically limited supply in the senior housing sector.

Key Takeaways

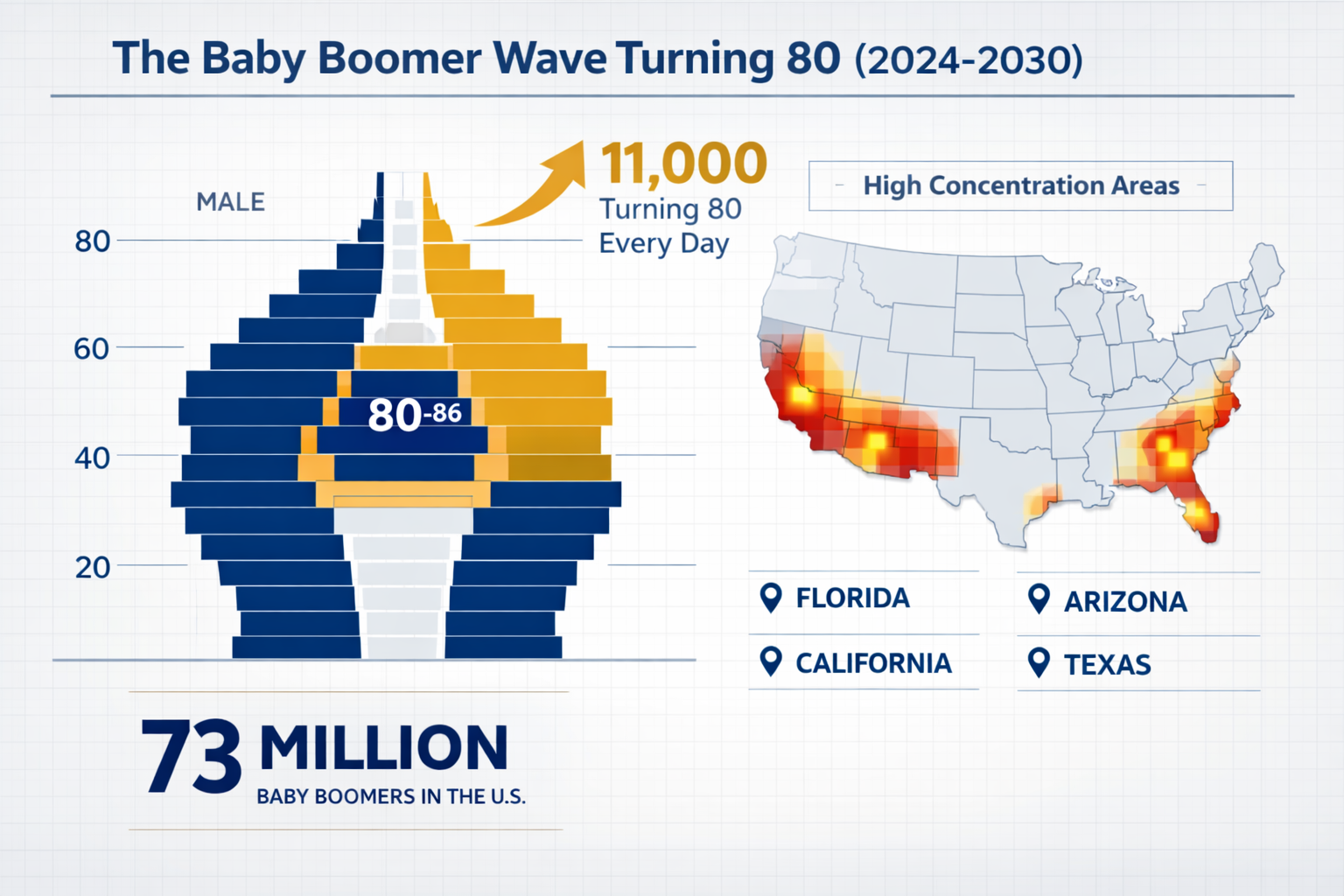

- 73 million Baby Boomers are driving explosive demand for senior housing as the oldest cohort reaches 80 in 2026

- Wellness-focused communities with tech-enabled amenities achieve occupancy rates of 92-96%, compared to 78-82% for traditional facilities

- Senior housing supply remains 15-20% below demand in high-growth markets like Phoenix, Tampa, and Charlotte

- Memory care facilities show the highest growth potential, with demand expected to triple by 2030

- Investment-grade senior housing properties deliver cap rates of 5-7% with strong rent growth potential

- Continuing Care Retirement Communities (CCRCs) offer the most stable cash flows but require higher initial capital

- Technology integration (telehealth, smart sensors, wearables) reduces operating costs by 12-18% while improving resident outcomes

- Secondary markets in the Sun Belt offer better value and higher yields than saturated coastal metros

- Regulatory complexity and staffing challenges remain the biggest operational risks for investors

- Joint ventures with experienced operators provide the best risk-adjusted returns for new senior housing investors

Quick Answer

The Senior Housing Boom 2026 creates exceptional investment opportunities as Baby Boomers turn 80, driving demand for modern senior living facilities that far exceeds current supply. Investors who focus on wellness-oriented, tech-enabled communities in high-growth markets can capture cap rates of 5-7% with strong appreciation potential, particularly in memory care and assisted living segments. The key to success lies in partnering with experienced operators who understand the regulatory landscape and can deliver the amenities today's seniors expect.

Why Is the Senior Housing Market Exploding in 2026?

The senior housing market is experiencing explosive growth in 2026 because the oldest Baby Boomers, born in 1946, are turning 80—the age when most Americans require some form of senior living assistance. This demographic wave creates approximately 11,000 new potential senior housing residents every single day.

The math is simple but powerful. Between 2026 and 2030, the population aged 80 and older will grow by roughly 35%, while the supply of senior housing units has increased by only 8-12% over the past five years. This supply-demand imbalance creates pricing power for property owners and operators.

Key demographic drivers include:

- 73 million Baby Boomers entering their highest-need years for senior services

- Increased life expectancy means longer stays in senior housing (average 3.5 years in assisted living, up from 2.8 years in 2015)

- Growing preference for aging in specialized communities rather than with family members

- Rising rates of Alzheimer's and dementia requiring specialized memory care facilities

- Wealth accumulation among Boomers providing ability to pay premium prices for quality accommodations

What makes 2026 particularly significant is that this isn't a temporary spike. The demographic wave continues for at least another decade, providing sustained demand that justifies long-term capital investment.

What Types of Senior Housing Offer the Best Investment Returns?

Independent Living, Assisted Living, Memory Care, and Continuing Care Retirement Communities (CCRCs) each offer distinct risk-return profiles, with memory care and assisted living currently delivering the strongest returns due to acute supply shortages.

Independent Living

Independent living communities serve active seniors who don't need daily assistance but want amenities, social activities, and maintenance-free living. These properties typically deliver:

- Cap rates of 4.5-6%

- Lower operating costs due to minimal care requirements

- Higher turnover risk as residents age into higher-care needs

- Best suited for prime locations near cultural amenities

Choose independent living if you want lower operational complexity and can accept moderate returns in exchange for reduced regulatory burden.

Assisted Living

Assisted living facilities provide daily support with activities like bathing, dressing, and medication management. This segment shows:

- Cap rates of 5.5-7%

- Strong demand growth of 6-8% annually

- Higher staffing costs but better retention rates

- Occupancy rates of 88-93% in well-managed properties

Common mistake: Underestimating staffing costs, which can consume 55-65% of operating revenue in assisted living.

Memory Care

Memory care units specialize in Alzheimer's and dementia patients, requiring secure environments and specialized staff training. Investment characteristics include:

- Cap rates of 6-7.5%

- Highest demand growth (projected 12-15% annually through 2030)

- Premium pricing power ($6,000-$9,000 monthly versus $4,500-$6,000 for standard assisted living)

- Specialized licensing and higher insurance costs

- Longest average stays (4-6 years)

Continuing Care Retirement Communities (CCRCs)

CCRCs offer a continuum from independent living through skilled nursing on one campus. These properties feature:

- Cap rates of 5-6.5%

- Most stable cash flows due to long-term contracts

- Highest barriers to entry (typically $500,000+ entrance fees plus monthly fees)

- Complex regulatory requirements

- Lowest resident turnover

Comparison Table:

| Property Type | Cap Rate | Occupancy | Monthly Cost | Demand Growth | Operational Complexity |

|---|---|---|---|---|---|

| Independent Living | 4.5-6% | 85-90% | $2,500-$4,500 | Moderate (3-5%) | Low |

| Assisted Living | 5.5-7% | 88-93% | $4,500-$6,000 | Strong (6-8%) | Medium |

| Memory Care | 6-7.5% | 90-96% | $6,000-$9,000 | Very Strong (12-15%) | High |

| CCRC | 5-6.5% | 92-95% | $3,000-$7,000 + entrance fee | Moderate (4-6%) | Very High |

How Are Wellness and Technology Transforming Senior Housing Investment Opportunities?

Wellness-focused, tech-enabled senior communities achieve occupancy rates 10-15 percentage points higher than traditional institutional facilities, directly impacting net operating income and property valuations. Modern seniors expect resort-style amenities and integrated technology that supports independence.

The transformation is dramatic. Traditional senior housing featured shared rooms, institutional dining halls, and limited activities. Today's high-performing communities offer:

Wellness amenities that drive occupancy:

- Professional fitness centers with senior-specific equipment and personal trainers

- Yoga, tai chi, and meditation studios

- Farm-to-table dining with chef-prepared meals and dietary customization

- Art studios, woodworking shops, and creative spaces

- Outdoor walking trails, gardens, and nature areas

- Spa services including massage, salon, and wellness treatments

Technology integration that reduces costs and improves outcomes:

- Telehealth systems enabling remote physician consultations (reduces emergency room visits by 25-30%)

- Smart sensors detecting falls, unusual movement patterns, or missed medications

- Wearable devices monitoring vital signs and activity levels

- Automated medication dispensing reducing errors and staffing needs

- Digital engagement platforms for family communication and activity scheduling

- Smart building systems optimizing energy use and maintenance

"Communities that invested $2-3 million in technology upgrades saw operating costs decrease by 12-18% within 18 months while simultaneously increasing occupancy from 82% to 94%." — Based on operational data from high-performing senior housing portfolios

Case study example: A 180-unit assisted living community in suburban Phoenix invested $2.8 million in wellness amenities (fitness center, chef's kitchen, art studio) and technology infrastructure (telehealth, sensors, wearables) in 2024. Within 14 months:

- Occupancy increased from 81% to 95%

- Average monthly rent rose from $4,800 to $5,400

- Staff turnover decreased from 68% to 42%

- Emergency medical incidents dropped 31%

- Net operating income increased 47%

The property's valuation increased by approximately $12 million on a $2.8 million investment, demonstrating the powerful returns from modernization.

Where Are the Highest-Growth Markets for Senior Housing in 2026?

Sun Belt secondary markets including Phoenix, Tampa, Charlotte, Raleigh, and Austin offer the best combination of demand growth, affordability, and yield for senior housing investors in 2026, outperforming saturated coastal metros.

Primary coastal markets like San Francisco, New York, and Boston face challenges:

- High land and construction costs ($400-$600 per square foot)

- Extensive regulatory requirements and lengthy approval processes

- Already saturated with senior housing inventory

- Cap rate compression to 4-5% in many submarkets

Top-performing markets for 2026 investment:

Phoenix, Arizona

- 65+ population growing 4.2% annually

- Construction costs 30-40% below coastal markets

- Strong in-migration of affluent retirees

- Cap rates: 5.5-6.5%

- Occupancy rates: 91-94%

Tampa-St. Petersburg, Florida

- No state income tax attracting retiree migration

- Year-round climate supporting outdoor wellness amenities

- Healthcare infrastructure with major medical centers

- Cap rates: 5.8-6.8%

- Occupancy rates: 89-93%

Charlotte, North Carolina

- Rapidly growing 75+ population (6.1% annually)

- Lower cost of living than Northeast markets

- Strong healthcare systems (Atrium Health, Novant)

- Cap rates: 6-7%

- Occupancy rates: 87-91%

Raleigh-Durham, North Carolina

- Highly educated retiree population

- Research Triangle healthcare excellence

- Four-season climate with mild winters

- Cap rates: 5.8-6.5%

- Occupancy rates: 88-92%

Austin, Texas

- Affluent retiree in-migration

- No state income tax

- Strong cultural amenities

- Cap rates: 5.5-6.2%

- Occupancy rates: 90-94%

Choose secondary Sun Belt markets if you want higher yields, lower entry costs, and strong demographic tailwinds. Choose primary coastal markets only if you have deep capital reserves and can accept lower yields for perceived stability.

What Are the Financial Metrics Investors Should Target in Senior Housing?

Successful senior housing investments in 2026 should target cap rates of 5.5-7%, occupancy rates above 90%, and revenue per occupied unit (RevPOR) growth of 3-5% annually, with careful attention to operating expense ratios and debt service coverage.

Critical Financial Metrics

Capitalization Rate (Cap Rate)

- Target: 5.5-7% for stabilized properties

- Memory care and assisted living at higher end

- Independent living and CCRCs at lower end

- Markets with strong demographics support cap rate compression over time

Occupancy Rate

- Target: 90%+ for stabilized properties

- Anything below 85% signals operational or market issues

- Occupancy is the single biggest driver of NOI in senior housing

- Lease-up properties may take 18-36 months to stabilize

Revenue Per Occupied Room (RevPOR)

- Track monthly and annually

- Target 3-5% annual growth through rate increases and ancillary services

- Compare to market averages by property type

- Strong RevPOR growth indicates pricing power

Operating Expense Ratio

- Target: 70-75% for assisted living and memory care

- Target: 60-65% for independent living

- Labor typically represents 55-65% of total expenses

- Watch for expense ratio creep indicating operational issues

Net Operating Income (NOI) Margin

- Target: 25-30% for well-managed properties

- Higher margins indicate operational efficiency

- Compare year-over-year trends

Debt Service Coverage Ratio (DSCR)

- Target: 1.25x or higher

- Lenders typically require minimum 1.20x

- Higher DSCR provides cushion for occupancy fluctuations

Underwriting Checklist

When evaluating a senior housing investment opportunity:

- Verify actual occupancy (not just "stabilized" pro forma)

- Review 3+ years of operating statements to identify trends

- Analyze rent roll for turnover patterns and rate structure

- Assess deferred maintenance and capital improvement needs

- Evaluate competitive set within 3-5 mile radius

- Review staffing levels and turnover rates (high turnover kills profitability)

- Confirm licensing and regulatory compliance status

- Analyze payor mix (private pay vs. Medicaid, if applicable)

- Model multiple exit scenarios at various cap rates

- Stress test for 10-15% occupancy decline

Common mistake: Accepting operator-provided pro forma projections without independent verification. Always underwrite conservatively using actual historical performance.

How Can Investors Enter the Senior Housing Market?

Investors can access the Senior Housing Boom 2026 through direct property ownership, joint ventures with experienced operators, senior housing REITs, or debt investments, with joint ventures offering the best risk-adjusted returns for most investors new to the sector.

Investment Structure Options

Direct Ownership

- Capital required: $5-50+ million depending on property size

- Best for: Experienced real estate investors with operational expertise

- Pros: Full control, highest potential returns, tax benefits

- Cons: Operational complexity, regulatory burden, staffing challenges

- Expected returns: 12-18% IRR for value-add opportunities

Joint Venture with Experienced Operator

- Capital required: $2-10+ million for equity stake

- Best for: Investors seeking senior housing exposure without operational headaches

- Pros: Leverage operator expertise, shared risk, learning opportunity

- Cons: Shared returns, less control, partner selection critical

- Expected returns: 10-15% IRR with experienced partners

- Structure: Typically 80/20 or 70/30 LP/GP split with preferred return

Senior Housing REITs

- Capital required: As little as $1,000 for publicly traded REITs

- Best for: Investors wanting liquidity and diversification

- Pros: Liquidity, professional management, diversification

- Cons: Lower returns, no control, market volatility

- Expected returns: 6-10% total return (dividends plus appreciation)

- Major REITs: Welltower, Ventas, Healthpeak Properties, Sabra Health Care

Debt Investments

- Capital required: $500,000+ for direct lending; lower for funds

- Best for: Conservative investors seeking current income

- Pros: Senior position in capital stack, predictable returns, lower risk

- Cons: Limited upside, foreclosure risk if borrower fails

- Expected returns: 7-10% for senior debt; 10-14% for mezzanine

Steps to Get Started

For investors with $2-10 million to deploy:

- Identify target markets based on demographics and supply-demand fundamentals

- Build relationships with 3-5 experienced operators in those markets

- Review their track records including historical occupancy, NOI growth, and exits

- Negotiate joint venture terms including preferred return (typically 7-9%), profit split, and decision rights

- Conduct thorough due diligence on specific opportunities

- Engage specialized legal counsel for operating agreements and regulatory compliance

- Structure financing (typically 60-70% LTV senior debt)

- Monitor performance monthly with detailed reporting from operator

For investors with under $2 million:

- Consider senior housing REITs for immediate exposure and liquidity

- Explore crowdfunding platforms specializing in senior housing (minimum investments $25,000-$100,000)

- Invest in senior housing debt funds for current income

- Build knowledge and relationships for future direct investment

Edge case: Some investors purchase smaller properties (20-40 units) in secondary markets for $3-8 million and hire third-party management. This can work but requires very careful operator selection and hands-on oversight.

What Are the Biggest Risks in Senior Housing Investment?

Regulatory complexity, staffing shortages, and occupancy volatility represent the three biggest risks for senior housing investors in 2026, though proper due diligence and experienced operators can mitigate these challenges significantly.

Major Risk Factors

Regulatory and Licensing Risk

- Senior housing faces extensive state and local regulations

- Licensing requirements vary dramatically by state and property type

- Violations can result in fines, license suspension, or closure

- Changes in regulations can require expensive retrofits

- Mitigation: Partner with operators who have spotless compliance records and strong relationships with regulators

Labor Shortages and Wage Inflation

- Healthcare workers are in short supply nationally

- Staff turnover rates of 50-70% are common in the industry

- Wage pressure increasing 4-6% annually

- Poor staffing leads to quality issues and occupancy decline

- Mitigation: Invest in properties with strong culture, competitive pay, and technology that reduces labor intensity

Occupancy Volatility

- Senior housing can experience rapid occupancy swings

- Economic downturns impact move-in rates

- Competing properties can steal market share

- A 10% occupancy drop can eliminate 30-40% of NOI

- Mitigation: Focus on markets with strong demand fundamentals and properties with differentiated amenities

Reimbursement Risk

- Properties accepting Medicaid face reimbursement rate risk

- Medicare Advantage changes can impact skilled nursing components

- Mitigation: Focus on private-pay properties or limit Medicaid exposure to under 20%

Construction and Development Risk

- New construction takes 18-30 months and faces cost overruns

- Lease-up risk during stabilization period

- Interest rate sensitivity during construction period

- Mitigation: Focus on stabilized acquisitions or value-add opportunities rather than ground-up development

Reputation and Liability Risk

- Negative reviews spread quickly online

- Falls, medication errors, or abuse allegations can destroy a property's reputation

- Litigation risk from resident families

- Mitigation: Invest only with operators who have excellent quality ratings and comprehensive insurance

Risk Mitigation Strategies

Diversification

- Spread investment across multiple properties and markets

- Mix property types (independent living, assisted living, memory care)

- Avoid concentration in single operator or geographic area

Conservative Underwriting

- Stress test for 10-15% occupancy decline

- Budget 3-5% annual expense growth

- Maintain DSCR of 1.25x or higher

- Reserve 5-7% of revenue for capital improvements

Operator Selection

- Require minimum 10 years operating experience

- Review quality ratings and inspection reports

- Check references from previous investors

- Ensure operator has skin in the game (equity investment)

Legal Structure

- Use special purpose entities for each property

- Maintain adequate insurance coverage

- Include strong operating agreements with performance metrics

- Build in exit rights if operator underperforms

What Does the Future Hold for Senior Housing Beyond 2026?

The Senior Housing Boom 2026: Investment Opportunities as Baby Boomers Turn 80 represents just the beginning of a multi-decade growth cycle, with demand expected to accelerate through 2035 as the entire Baby Boomer generation ages into their 80s and 90s.

Long-Term Trends Shaping the Industry

Continued Demographic Tailwinds

- The 80+ population will grow from approximately 13 million in 2026 to over 20 million by 2035

- This represents sustained 4-6% annual growth in the target demographic

- The trend continues for at least 15 more years, providing long-term investment visibility

Technology Integration Acceleration

- Artificial intelligence will enable predictive health monitoring

- Robotics will assist with routine tasks and reduce labor dependency

- Virtual reality will provide cognitive stimulation and entertainment

- Smart home technology will extend independent living capabilities

- Properties without technology integration will become obsolete

Shift Toward Hospitality Model

- Senior living will increasingly resemble luxury hospitality

- Michelin-quality dining, concierge services, and curated experiences

- Intergenerational programming and community integration

- Wellness and prevention focus rather than just care

- Properties that feel institutional will struggle to compete

Affordability Challenges

- Middle-market seniors (too wealthy for Medicaid, too poor for luxury) face limited options

- Opportunity for innovative models serving the "missing middle"

- Potential for government subsidies or insurance products

- Shared housing and co-housing models may emerge

Climate and Location Preferences

- Continued migration to Sun Belt and climate-resilient areas

- Proximity to family becoming more important than climate for some

- Urban senior housing gaining popularity among city-dwelling Boomers

- Suburban locations near medical centers remain strong

Consolidation and Institutionalization

- Larger operators and REITs will acquire smaller portfolios

- Private equity will continue flowing into the sector

- Mom-and-pop operators will struggle to compete

- Economies of scale in purchasing, technology, and staffing

Investment Outlook Through 2035

The senior housing sector offers one of the most compelling long-term investment theses in commercial real estate:

- Sustained demand growth from demographics

- Limited new supply due to development challenges

- Pricing power from supply-demand imbalance

- Inflation protection through regular rate increases

- Recession resilience as seniors have limited housing alternatives

Investors who enter the market in 2026 with quality properties, experienced operators, and proper capitalization should see strong risk-adjusted returns for the next decade and beyond.

The key question isn't whether to invest in senior housing, but how to position for maximum advantage in what may be the commercial real estate opportunity of the next 20 years.

Frequently Asked Questions

What makes 2026 special for senior housing investment?

2026 marks the year the oldest Baby Boomers turn 80, the age when most Americans require senior living assistance. This creates a demographic surge of approximately 11,000 new potential residents daily, driving unprecedented demand against limited supply.

How much money do I need to invest in senior housing?

Direct property ownership typically requires $5-50 million, while joint ventures with operators may accept $2-10 million. Senior housing REITs allow investment starting at just a few thousand dollars, and crowdfunding platforms often have minimums of $25,000-$100,000.

What returns can I expect from senior housing investment?

Expected returns vary by structure: direct ownership value-add deals may deliver 12-18% IRR, joint ventures typically target 10-15% IRR, REITs historically provide 6-10% total returns, and debt investments offer 7-14% depending on position in the capital stack.

Is senior housing recession-resistant?

Senior housing shows more resilience than other commercial real estate because seniors have limited alternatives once they require care. However, economic downturns can slow move-in rates and pressure pricing, particularly for independent living where care needs are less acute.

What's the difference between assisted living and memory care?

Assisted living provides help with daily activities like bathing, dressing, and medication for seniors who don't need 24/7 medical care. Memory care specializes in Alzheimer's and dementia patients, requiring secure environments, specialized staff training, and higher staff-to-resident ratios, which commands premium pricing.

Should I invest in new construction or existing properties?

Existing stabilized properties offer lower risk with immediate cash flow but limited upside. New construction or value-add properties offer higher potential returns but carry lease-up risk, construction delays, and cost overruns. Most investors should start with stabilized properties to learn the business.

What occupancy rate should I target?

Target 90%+ occupancy for stabilized properties. Anything below 85% suggests operational or market problems. During lease-up, properties may take 18-36 months to reach stabilization, so underwrite conservative ramp-up periods.

How do I find experienced senior housing operators to partner with?

Attend industry conferences like Argentum and NIC, network with senior housing brokers who work with operators, research operators in your target markets through state licensing databases, and request introductions from commercial real estate attorneys who specialize in senior housing.

What are the tax advantages of senior housing investment?

Senior housing qualifies for depreciation deductions (typically 27.5-39 year schedules), potential 1031 exchange treatment for tax-deferred gains, opportunity zone benefits in qualifying areas, and pass-through deductions for partnerships. Consult a tax advisor for your specific situation.

Can I use a self-directed IRA to invest in senior housing?

Yes, self-directed IRAs can invest in senior housing through direct property ownership, joint ventures, or private placements. However, strict rules prohibit self-dealing, and all income and expenses must flow through the IRA. Work with a self-directed IRA custodian experienced in real estate.

What happens if occupancy drops significantly?

A 10% occupancy decline can eliminate 30-40% of NOI since fixed costs remain constant. Maintain DSCR of 1.25x or higher to weather occupancy volatility, keep adequate reserves (6-12 months operating expenses), and stress test underwriting for 10-15% occupancy drops.

How long should I plan to hold a senior housing investment?

Most investors target 5-10 year hold periods to allow for value creation, market appreciation, and favorable exit timing. Senior housing requires longer holds than other commercial real estate due to operational complexity and the time needed to stabilize and optimize properties.

Conclusion

The Senior Housing Boom 2026: Investment Opportunities as Baby Boomers Turn 80 represents a generational wealth-creation opportunity driven by powerful demographics, limited supply, and evolving resident expectations. As 73 million Baby Boomers age into their highest-need years, investors who position themselves strategically in wellness-focused, tech-enabled communities can capture exceptional risk-adjusted returns.

The data is compelling: 11,000 Americans turning 80 every day, supply shortages of 15-20% in high-growth markets, occupancy rates exceeding 90% in modern facilities, and cap rates of 5-7% with strong appreciation potential. Memory care and assisted living offer the highest growth potential, while secondary Sun Belt markets provide better value than saturated coastal metros.

Success in senior housing investment requires more than capital. It demands careful market selection, partnership with experienced operators who understand regulatory complexity and staffing challenges, and commitment to the amenities and technology that today's seniors expect. Properties that feel institutional will struggle, while those offering resort-style wellness amenities and integrated technology will thrive.

Next Steps for Prospective Investors

If you're ready to explore senior housing investment:

- Educate yourself on the different property types and their risk-return profiles

- Identify 2-3 target markets based on demographics, supply-demand, and your investment criteria

- Build relationships with experienced operators through industry conferences, brokers, and networking

- Start small with a joint venture or REIT investment to learn the business before committing major capital

- Assemble your team including specialized legal counsel, accountants familiar with senior housing, and commercial brokers

- Conduct thorough due diligence on any opportunity, verifying all operator claims independently

- Underwrite conservatively with stress tests for occupancy declines and expense growth

- Monitor performance closely with monthly reporting and regular property visits

The senior housing sector will continue growing for at least the next 15 years as Baby Boomers age through their 80s and 90s. Investors who enter the market now with proper preparation, experienced partners, and quality properties should see strong returns throughout this multi-decade growth cycle.

The opportunity is clear. The demographic wave is unstoppable. The question is whether you'll position yourself to benefit from one of the most compelling investment themes of the next two decades.