Navigating the 2026 Capital Markets Fog: Strategies for Real Estate Investors Facing Economic Uncertainty

The commercial real estate market in 2026 sits at a crossroads. Navigating the 2026 Capital Markets Fog: Strategies for Real Estate Investors Facing Economic Uncertainty requires a clear-eyed approach to higher financing costs, compressed yields, and the renewed price discovery process

Last updated: February 24, 2026

The commercial real estate market in 2026 sits at a crossroads. Navigating the 2026 Capital Markets Fog: Strategies for Real Estate Investors Facing Economic Uncertainty requires a clear-eyed approach to higher financing costs, compressed yields, and the renewed price discovery process reshaping property valuations across all asset classes. Investors who adapt their strategies to this environment can uncover opportunities that others miss.

Key Takeaways

- Financing costs remain elevated in 2026, with commercial mortgage rates hovering between 6.5-8%, forcing investors to recalibrate return expectations and underwriting models

- Price discovery is accelerating as sellers accept the new interest rate reality, creating opportunities for patient capital with strong balance sheets

- Core assets in gateway markets are showing resilience with stable occupancy and rent growth, offering defensive positioning during economic uncertainty

- Debt service coverage ratios have become the critical metric, with lenders requiring minimum 1.25x DSCR compared to 1.15x in previous cycles

- Alternative property sectors including industrial, life sciences, and data centers continue outperforming traditional office and retail

- Bridge-to-core strategies allow investors to capture value-add returns while positioning for long-term holds as markets stabilize

- Geographic diversification across primary and secondary markets reduces concentration risk in an uncertain economic environment

- Flexible capital structures combining equity, preferred equity, and mezzanine debt provide cushion against valuation volatility

Quick Answer

Real estate investors facing the 2026 capital markets fog should focus on core assets with strong fundamentals, maintain conservative leverage (50-60% LTV), and prioritize cash flow stability over speculative appreciation. The elevated financing environment demands disciplined underwriting with stress-tested scenarios for interest rates, occupancy, and exit cap rates. Opportunities exist in sectors with structural tailwinds and in situations where sellers have accepted the new pricing reality, but success requires patient capital and operational expertise.

What Is Causing the 2026 Capital Markets Fog for Real Estate Investors?

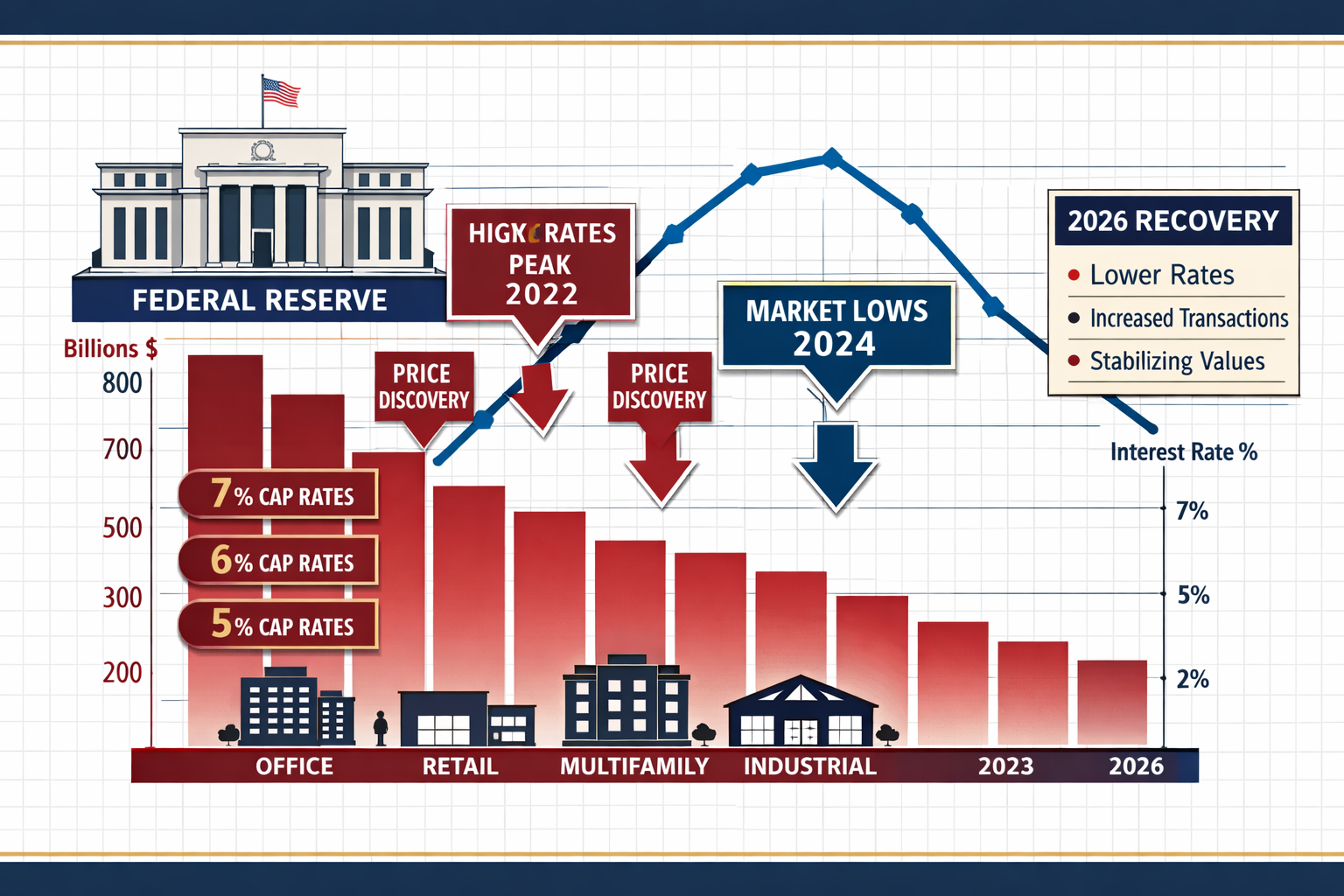

The capital markets fog in 2026 stems from persistent interest rate uncertainty, banking sector caution following regional bank stress in 2023-2024, and the ongoing repricing of commercial real estate values. After the Federal Reserve raised rates aggressively in 2022-2023, the market entered a period where buyers and sellers disagreed on valuations, creating a transaction volume drought.

Three primary factors drive the current uncertainty:

- Interest rate environment - Even with potential rate cuts on the horizon, commercial mortgage rates remain 300-400 basis points higher than 2021 levels, fundamentally changing investment returns

- Banking sector pullback - Regional and community banks, historically providing 40-50% of commercial real estate loans, have tightened lending standards and reduced exposure

- Maturity wall concerns - Approximately $1.5 trillion in commercial real estate debt matures between 2024-2027, creating refinancing pressure for overleveraged properties

The fog metaphor fits because visibility into future conditions remains limited. Economic indicators send mixed signals: employment remains relatively strong in many markets, but consumer spending shows signs of fatigue. Office fundamentals continue struggling with remote work adoption, while industrial and multifamily sectors demonstrate resilience.

Choose defensive positioning if your portfolio lacks liquidity or you're heavily concentrated in struggling sectors. Choose opportunistic strategies if you have dry powder and can underwrite to today's higher cost of capital without relying on rate compression for returns.

A common mistake is waiting for a return to 2021 conditions. That low-rate environment was an anomaly, not a baseline. Investors who accept the new normal and adjust their return expectations accordingly will find opportunities while others remain sidelined.

How Are Higher Financing Costs Reshaping Real Estate Investment Decisions in 2026?

Higher financing costs have fundamentally altered the investment calculus for commercial real estate in 2026. With all-in borrowing costs ranging from 6.5% to 8% depending on property type and leverage, the spread between cap rates and debt costs has compressed dramatically compared to the 2010-2021 period.

The impact shows up in several critical areas:

Leverage decisions - Investors are targeting 50-60% loan-to-value ratios instead of the 65-75% common in previous cycles. Lower leverage reduces cash-on-cash returns but provides crucial cushion against valuation declines and creates flexibility if refinancing conditions worsen.

Hold period assumptions - The traditional 5-7 year hold period is extending to 7-10 years for many value-add deals. Investors need more time to execute business plans and wait for potential cap rate compression before exiting profitably.

Cash flow emphasis - Speculative appreciation plays have given way to cash flow-focused strategies. Properties must generate sufficient net operating income to cover debt service with healthy margins. The days of buying negative cash flow properties betting on rapid rent growth are largely over.

Equity return expectations - Levered equity returns in the 12-15% range are replacing the 18-25% targets common when debt was cheap. Investors who cannot adjust their return hurdles will struggle to deploy capital.

| Metric | 2021 Environment | 2026 Environment | Impact |

|---|---|---|---|

| Mortgage Rate | 3.0-4.0% | 6.5-8.0% | Higher debt service |

| Typical LTV | 65-75% | 50-60% | More equity required |

| DSCR Requirement | 1.15x | 1.25-1.35x | Tighter underwriting |

| Avg Hold Period | 5-7 years | 7-10 years | Longer capital lockup |

| Target Equity IRR | 18-25% | 12-15% | Compressed returns |

Choose all-cash or low-leverage strategies if you're acquiring properties with near-term lease rollover risk or in markets with uncertain demand fundamentals. Choose moderate leverage (50-60% LTV) if you're buying stabilized core assets with long-term leases and creditworthy tenants.

The biggest mistake is underwriting to optimistic refinancing assumptions. Stress test your deals assuming rates stay elevated or even increase. If the investment only works with rate cuts and cap rate compression, it's probably too risky for the current environment.

What Opportunities Exist in Core Assets During This Period of Price Discovery?

Core assets in primary markets are emerging as the sweet spot for navigating the 2026 capital markets fog. Price discovery is finally happening as sellers accept that the low cap rates of 2021-2022 are not returning anytime soon, creating entry points for patient capital.

Core assets offer several advantages in uncertain times:

Predictable cash flows - Class A properties with creditworthy tenants on long-term leases provide the stability investors crave when economic visibility is low. These assets can weather recessions better than value-add or opportunistic plays.

Financing availability - While debt markets have tightened overall, lenders still compete for high-quality core assets. Life insurance companies, CMBS, and agency lenders continue providing attractive terms for trophy properties.

Inflation hedge characteristics - Many core assets include rent escalators tied to CPI or have lease structures allowing for regular rent resets, providing some protection against persistent inflation.

Flight to quality dynamics - During uncertain periods, capital concentrates in the safest assets. This phenomenon can actually compress cap rates on core properties even as riskier assets see cap rate expansion.

Specific opportunities in 2026 include:

- Gateway market multifamily - Class A apartments in supply-constrained coastal markets with strong employment and limited new construction pipelines

- Last-mile industrial - Modern logistics facilities in major distribution markets with long-term leases to investment-grade tenants

- Life sciences clusters - Purpose-built lab space in established biotech hubs like Boston, San Francisco, and San Diego

- Essential retail - Grocery-anchored shopping centers and necessity-based retail in affluent trade areas

The key is finding situations where sellers have realistic pricing expectations. Look for properties that have been on the market 6-12 months with price reductions, estate sales requiring liquidity, or institutional sellers rebalancing portfolios.

Choose core assets if you prioritize capital preservation and steady income over maximum returns, or if you're investing for institutions with long time horizons. Avoid core assets if you need high teens returns or have a short investment horizon, as these properties rarely offer explosive appreciation.

A common edge case: some "core" assets in secondary markets actually offer better risk-adjusted returns than gateway market properties because pricing hasn't fully adjusted yet. A Class A apartment building in Nashville or Austin might offer 100-150 basis points more yield than a comparable San Francisco property with similar quality tenants.

How Should Investors Adjust Their Underwriting Models for Economic Uncertainty?

Conservative underwriting separates successful investors from those who get caught in the capital markets fog. In 2026, models must account for scenarios that seemed unlikely during the low-rate era: rising vacancies, declining rents, higher operating expenses, and limited exit options.

Essential underwriting adjustments for 2026:

Stress test multiple scenarios - Run at least three cases: base (most likely), downside (mild recession), and severe downside (significant economic contraction). Your deal should still generate acceptable returns in the downside case.

Conservative rent growth assumptions - Use 2-3% annual rent growth instead of the 4-6% projections common in hot markets during 2021-2022. For office properties, consider flat or negative rent growth given structural headwinds.

Realistic exit cap rates - Assume exit cap rates 50-100 basis points higher than entry cap rates. The days of underwriting to cap rate compression are over. If your deal requires a lower exit cap rate to hit return targets, it's too risky.

Higher operating expense growth - Budget for 4-5% annual expense growth, particularly for insurance, property taxes, and utilities. These categories have seen above-average inflation and show no signs of moderating.

Debt service coverage buffers - Target minimum 1.30x DSCR even if lenders will accept 1.25x. This cushion protects against unexpected income drops or expense spikes.

Shorter interest-only periods - Don't rely on long IO periods to boost returns. Underwrite to amortizing debt from year one, treating any IO as a bonus that improves cash flow.

Checklist for robust 2026 underwriting:

- Vacancy assumptions at or above submarket averages (no "better than market" optimism)

- Renewal probability rates based on actual property history, not aspirational targets

- Market rent growth tied to employment and population growth forecasts

- Capital expenditure reserves of $0.20-0.40/SF annually for stabilized properties

- Tenant improvement and leasing commission costs at current market rates, not historical averages

- Property tax appeals factored in only if already filed and likely to succeed

- Exit assumptions assuming today's market conditions persist (no rate cut benefit)

- Sensitivity analysis showing returns across range of outcomes

Choose aggressive assumptions only if you have contractual protections like long-term leases, rent guarantees, or master lease structures that eliminate market risk. Choose conservative assumptions if you're using significant leverage, investing in volatile markets, or lack operational expertise to execute complex business plans.

The most dangerous mistake is anchoring to pre-2022 underwriting standards. Models that worked when debt was 3% and cap rates were compressing will destroy capital in today's environment. Investors who survived previous downturns know that conservative underwriting during uncertain times preserves capital and positions you to capitalize when clarity returns.

What Role Do Alternative Property Sectors Play in Portfolio Diversification?

Alternative property sectors offer diversification benefits and often better risk-adjusted returns than traditional office, retail, and multifamily assets in 2026. These sectors include industrial, data centers, life sciences, self-storage, medical office, and specialized niches with structural demand drivers.

Why alternatives deserve attention during market uncertainty:

Lower correlation to economic cycles - Data centers and cell towers generate revenue from long-term contracts largely independent of GDP growth. Self-storage demand actually increases during economic stress as people downsize.

Structural growth trends - E-commerce drives industrial demand, aging demographics support medical office and senior housing, and cloud computing fuels data center absorption. These trends persist regardless of short-term economic fluctuations.

Limited new supply - Many alternative sectors have high barriers to entry (technical requirements, zoning restrictions, specialized expertise) that constrain new development and protect existing assets.

Institutional-quality tenants - Life sciences properties lease to pharmaceutical companies and research institutions. Data centers serve tech giants and cloud providers. These tenants typically have stronger credit profiles than traditional retail or office users.

Performance comparison across sectors in 2026:

| Sector | Avg Cap Rate | Occupancy Trend | Rent Growth | Risk Level |

|---|---|---|---|---|

| Industrial | 5.0-6.5% | Stable to rising | 3-5% | Low-Moderate |

| Data Centers | 6.0-7.5% | Rising | 4-6% | Moderate |

| Life Sciences | 5.5-7.0% | Stable | 2-4% | Moderate |

| Self-Storage | 6.5-8.0% | Stable | 2-3% | Moderate |

| Medical Office | 6.0-7.5% | Stable | 2-3% | Low-Moderate |

| Traditional Office | 6.5-9.0% | Declining | -2-0% | High |

| Retail (non-grocery) | 6.5-8.5% | Stable | 1-2% | Moderate-High |

Diversification strategies for 2026:

Core-plus industrial - Modern logistics facilities in secondary markets offer 100-150 basis points more yield than gateway markets with similar tenant quality and lease terms.

Medical office near major hospitals - These properties benefit from healthcare spending growth and physician practices that rarely relocate, providing stable cash flows.

Climate-controlled self-storage - Facilities in growing Sunbelt markets with dense populations offer strong unit-level economics and operational upside for experienced operators.

Life sciences in established clusters - Purpose-built lab space commands premium rents and attracts long-term tenants, but requires specialized knowledge and higher capital investment.

Choose alternative sectors if you have operational expertise or can partner with specialists, and you're seeking diversification from traditional property types. Avoid alternatives if you lack sector-specific knowledge, can't access deal flow in these competitive niches, or need high liquidity (these assets often have smaller buyer pools).

An important consideration: not all alternative sectors are created equal. Student housing and hospitality, sometimes classified as alternatives, carry significant operational complexity and economic sensitivity. Focus on sectors with structural tailwinds and predictable cash flows rather than chasing yield in operationally intensive niches.

How Can Investors Structure Deals to Protect Against Downside Risk?

Defensive deal structuring protects capital during the 2026 market fog while preserving upside participation when conditions improve. The right capital structure can mean the difference between surviving a downturn and facing foreclosure or distressed sales.

Key protective strategies for 2026 transactions:

Conservative leverage - Target 50-60% LTV on stabilized assets and 40-50% on value-add deals. Lower leverage provides cushion against valuation declines and ensures positive cash flow even if occupancy or rents slip.

Fixed-rate debt - Lock in long-term fixed rates even if they're 50-75 basis points higher than floating options. Interest rate risk is real, and the cost of hedging is worth the certainty.

Longer loan terms - Seek 7-10 year fully amortizing loans or 10-year terms with 25-30 year amortization. This minimizes refinancing risk and ensures you're not forced to sell into a bad market.

Flexible prepayment options - Negotiate step-down prepayment penalties or defeasance structures that allow you to exit if conditions improve or you find a better opportunity.

Cash reserves - Maintain 12-18 months of debt service in reserves, not the minimum 6 months lenders require. This buffer allows you to weather temporary income disruptions without defaulting.

Equity waterfalls with catch-ups - Structure GP/LP agreements with preferred returns (8-10%) and GP catch-up provisions that align interests while protecting LP downside.

Protective provisions for LPs:

- Approval rights on refinancing, major capital expenditures, and asset sales

- Regular reporting requirements (quarterly financials, annual budgets, monthly rent rolls)

- Removal rights if property performance falls below defined thresholds

- Co-investment requirements ensuring GP has meaningful skin in the game

Partnership structures that reduce risk:

Joint ventures with operators - Partner with experienced local operators who contribute expertise and some equity while you provide majority capital. This reduces execution risk on complex business plans.

Preferred equity positions - Instead of senior debt or common equity, consider preferred equity at 10-13% returns with downside protection and upside participation.

Programmatic partnerships - Commit capital to proven sponsors across multiple deals rather than concentrating in single assets, diversifying execution risk.

Choose aggressive structures only if you're buying significantly below replacement cost, have locked-in cash flows through long-term leases, or have multiple exit strategies. Choose defensive structures if you're uncertain about economic conditions, entering unfamiliar markets, or using investor capital with fiduciary obligations.

The critical mistake is optimizing for maximum leverage and returns without considering downside scenarios. The 2008-2010 crisis taught that overleveraged deals with short-term debt and optimistic assumptions destroy more wealth than any upside they capture. In foggy markets, the investors who survive are those who can weather storms, not those who maximize returns in the base case.

What Geographic and Market Selection Strategies Work Best in Uncertain Times?

Geographic diversification and careful market selection provide crucial risk management in 2026's uncertain environment. Not all markets face the same headwinds, and identifying locations with structural advantages separates successful portfolios from struggling ones.

Market characteristics that signal resilience:

Employment diversity - Markets with varied employment bases (healthcare, education, government, technology, finance) weather economic downturns better than single-industry towns. Austin, Boston, and Raleigh-Durham exemplify this diversity.

Population growth trends - Markets with positive net migration, particularly of working-age adults, support housing demand and commercial space absorption. Sunbelt markets continue attracting residents from high-cost coastal cities.

Business-friendly environments - Low taxes, reasonable regulations, and pro-growth policies attract companies and jobs. This matters more during uncertain times when businesses scrutinize location decisions.

Supply constraints - Markets with geographic limitations, strict zoning, or high development costs protect existing properties from oversupply. Coastal California cities and island markets like Honolulu have natural constraints.

Infrastructure investment - Markets receiving federal infrastructure spending, new transit systems, or major corporate relocations benefit from long-term tailwinds regardless of short-term economic conditions.

2026 market tier strategies:

Gateway markets (New York, Los Angeles, San Francisco, Boston, Washington DC)

- Pros: Deep liquidity, institutional-quality assets, diverse economies, limited supply

- Cons: High entry costs, compressed yields, significant competition

- Best for: Core strategies, capital preservation, investors needing liquidity

High-growth Sunbelt (Austin, Nashville, Raleigh, Charlotte, Phoenix)

- Pros: Strong population growth, business relocations, new construction absorption

- Cons: Cyclical volatility, potential oversupply in some sectors, less mature markets

- Best for: Core-plus and value-add strategies, growth-oriented investors

Secondary markets (Indianapolis, Columbus, Salt Lake City, Boise)

- Pros: Better yields, less competition, strong fundamentals, affordability

- Cons: Smaller buyer pools, less liquidity, fewer institutional-quality assets

- Best for: Value-add strategies, investors with local expertise, yield-focused buyers

Tertiary markets (smaller metros and suburban locations)

- Pros: Highest yields, least competition, niche opportunities

- Cons: Significant liquidity risk, limited debt options, higher execution risk

- Best for: Opportunistic strategies, local operators, specialized niches

Diversification approaches:

Geographic spread - Allocate across 3-5 markets in different regions to reduce concentration risk. A portfolio split between Sunbelt growth markets and stable Midwest metros balances growth and stability.

Market tier mixing - Combine gateway market core assets (30-40% of portfolio) with secondary market value-add deals (40-50%) and selective tertiary opportunities (10-20%).

Sector-market matching - Place industrial in logistics hubs, life sciences in research clusters, multifamily in job growth markets, and self-storage in dense suburban areas.

Choose gateway markets if you prioritize liquidity and capital preservation over maximum returns, or you're investing institutional capital with size requirements. Choose secondary/tertiary markets if you have local expertise, can accept illiquidity, and target higher returns with corresponding higher risk.

A valuable insight: the best opportunities in 2026 often exist in markets that were overlooked during the 2020-2022 boom. While everyone chased Austin and Nashville deals at compressed cap rates, markets like Indianapolis, Columbus, and Des Moines maintained reasonable pricing and now offer better risk-adjusted returns with less downside risk.

How Should Real Estate Investors Think About Timing and Deployment Strategy?

Timing capital deployment in the 2026 fog requires balancing the risk of sitting on the sidelines against the risk of catching a falling knife. The right approach depends on your capital source, return requirements, and conviction about market direction.

Deployment strategies for different investor types:

Opportunistic/all-cash investors - Deploy capital selectively into distressed or motivated seller situations offering 20-30% discounts to replacement cost. Wait for clear signs of distress rather than trying to time the bottom perfectly.

Core/core-plus investors - Dollar-cost average into stabilized assets over 12-24 months, taking advantage of price discovery as it happens. Avoid trying to time the market; focus on acquiring quality assets at reasonable yields.

Value-add investors - Be selective and patient. The best value-add opportunities emerge 12-18 months into a downturn when overleveraged owners face refinancing pressure. Build relationships with lenders and brokers to access off-market distress.

Fund managers with deployment deadlines - Negotiate extensions with LPs if possible, or focus on defensive core-plus deals that generate current income while waiting for better opportunities. Avoid forcing capital into mediocre deals just to meet deployment targets.

Indicators that suggest deployment timing:

Positive signals (time to deploy):

- Transaction volume increasing quarter-over-quarter

- Bid-ask spreads narrowing to 5-10% from 15-20%

- Sellers accepting price reductions and realistic valuations

- Debt markets reopening with reasonable terms

- Cap rates stabilizing after period of expansion

Negative signals (stay patient):

- Continuing transaction volume declines

- Wide bid-ask spreads with few trades

- Sellers still anchored to 2021-2022 pricing

- Debt markets frozen or requiring excessive equity

- Economic indicators deteriorating (rising unemployment, declining consumer spending)

Phased deployment approach:

Phase 1 (Months 1-6): Deploy 20-30% of capital into highest-conviction opportunities with strong downside protection. Focus on core assets with locked-in cash flows.

Phase 2 (Months 7-12): Deploy another 30-40% as market conditions clarify. Begin considering value-add opportunities if distress emerges.

Phase 3 (Months 13-24): Deploy remaining capital into best risk-adjusted opportunities based on market conditions. Maintain 10-15% reserve for unexpected opportunities.

Choose aggressive deployment if you see clear distress, have all-cash capability, and can underwrite conservatively to current conditions without relying on market improvement. Choose patient deployment if you're using leverage, lack conviction about market direction, or have flexible deployment timelines.

The most common mistake is deploying capital too quickly early in a correction, leaving no dry powder for better opportunities that emerge later. The second-most common mistake is waiting for the perfect bottom and missing the entire recovery. The solution is disciplined, phased deployment focused on risk-adjusted returns rather than trying to perfectly time the market.

What Are the Key Metrics and Benchmarks to Monitor in 2026?

Successful navigation of the 2026 capital markets fog requires monitoring the right indicators. These metrics provide early warning signals of changing conditions and help investors make informed decisions about acquisitions, holds, and dispositions.

Capital markets metrics:

10-Year Treasury yield - The foundation for all real estate pricing. Watch for sustained moves above 5% (negative for real estate) or below 3.5% (positive). Current levels around 4-4.5% represent the "new normal."

Credit spreads - The spread between corporate bonds and Treasuries indicates risk appetite. Widening spreads (above 200 bps for investment-grade) signal flight to safety and tighter lending conditions.

CMBS spreads - Commercial mortgage-backed securities spreads over swaps show debt market health. Spreads above 250 bps indicate stress; below 150 bps suggests healthy lending conditions.

Transaction volume - Year-over-year changes in sales volume indicate market liquidity. Volume down 40%+ suggests frozen markets; volume up 20%+ indicates improving conditions.

Property-level metrics:

Net operating income (NOI) growth - Track quarterly NOI growth across your portfolio and compare to market averages. Positive growth provides cushion; declining NOI requires action.

Occupancy rates - Monitor both physical and economic occupancy. Watch for divergence (high physical occupancy but low economic occupancy suggests rent collection problems).

Tenant retention - Renewal rates below 70% signal problems with property quality, management, or market fundamentals. Above 80% indicates strong tenant satisfaction.

Rent growth - Compare asking rents to in-place rents and to prior year. Negative rent growth on renewals is an early warning sign.

Market-level metrics:

Employment growth - Monthly job gains/losses in your target markets. Three consecutive months of job losses signals potential trouble.

Absorption rates - Net absorption (new leasing minus move-outs) indicates demand strength. Negative absorption for 2+ quarters suggests oversupply or weakening demand.

Construction pipeline - Monitor permits, starts, and deliveries. Supply exceeding absorption by 20%+ indicates potential oversupply.

Cap rate trends - Track cap rates by property type and market. Rising cap rates signal falling values; stable cap rates suggest price discovery is complete.

Benchmarking your portfolio:

| Metric | Strong Performance | Acceptable | Concerning | Action Required |

|---|---|---|---|---|

| NOI Growth YoY | >5% | 2-5% | 0-2% | <0% |

| Occupancy | >95% | 90-95% | 85-90% | <85% |

| Tenant Retention | >85% | 75-85% | 65-75% | <65% |

| DSCR | >1.50x | 1.30-1.50x | 1.20-1.30x | <1.20x |

| Rent Growth | >4% | 2-4% | 0-2% | <0% |

Choose aggressive growth strategies if your markets show strong employment growth, positive absorption, and rising rents. Choose defensive strategies if you see deteriorating fundamentals, rising vacancies, or negative rent growth.

The critical insight is that lagging indicators (transaction volume, cap rates) tell you what already happened, while leading indicators (employment, absorption, rent growth) tell you what's coming. Successful investors monitor both but make decisions based on leading indicators.

Frequently Asked Questions

What is the biggest risk facing real estate investors in 2026?

Refinancing risk poses the biggest threat for overleveraged properties purchased in 2020-2022. With debt maturing at 3-4% rates and refinancing at 6.5-8%, many properties cannot support the higher debt service without significant value destruction or equity infusions.

Are we at the bottom of the commercial real estate market in 2026?

Price discovery is still ongoing in many markets and sectors. Office properties likely have further downside, while industrial and multifamily have stabilized in most markets. Rather than trying to call the bottom, focus on buying assets that generate acceptable returns at today's prices without requiring market improvement.

What cap rates should investors target in 2026?

Target cap rates depend on property type and market, but generally 6-8% for core assets and 7-9% for value-add deals provide adequate spreads over debt costs. The key is ensuring positive leverage (cap rate exceeds mortgage rate) or accepting negative leverage in exchange for significant growth potential.

Is now a good time to sell commercial real estate?

Selling in 2026 makes sense if you bought before 2020 and have significant embedded gains, if your property faces structural headwinds (office, struggling retail), or if you're approaching debt maturity and cannot refinance on acceptable terms. Hold if you have locked-in low-rate debt and strong cash flows.

How much cash reserve should real estate investors maintain?

Maintain 12-18 months of debt service in reserves for leveraged properties, or 6-12 months of operating expenses for all-cash holdings. This cushion allows you to weather temporary disruptions and take advantage of opportunities without forced sales.

What property types should investors avoid in 2026?

Avoid commodity office buildings without unique characteristics, struggling retail centers without grocery anchors, and any property type where you lack operational expertise. Also avoid markets with significant oversupply or single-industry economies facing headwinds.

Can you still make money in real estate with high interest rates?

Yes, but the strategy shifts from leveraged appreciation plays to cash flow-focused investments. Target properties with in-place yields that exceed your debt costs, focus on operational improvements, and use moderate leverage (50-60% LTV) rather than maximum leverage.

What's the difference between core, core-plus, value-add, and opportunistic real estate strategies?

Core properties are stabilized, high-quality assets requiring minimal management (think Class A buildings with long-term leases). Core-plus assets need light improvements or have some lease rollover. Value-add properties require significant repositioning, renovations, or lease-up. Opportunistic investments include development, major redevelopment, or distressed assets requiring complete transformation.

How do you evaluate a real estate sponsor or operator?

Review their track record through full market cycles (not just 2010-2020 bull market), check references with past investors, verify their reported returns with third-party audits, assess their alignment of interest (meaningful co-investment), and evaluate their operational capabilities in your target property type.

Should investors wait for interest rates to fall before buying real estate?

No. Waiting for rate cuts means competing with everyone else who had the same idea, likely paying higher prices that offset any benefit from lower rates. Better to buy quality assets at fair prices today than to wait for potentially better financing but definitely higher competition.

What role should real estate play in an investment portfolio in 2026?

Real estate should comprise 10-30% of a diversified portfolio depending on your risk tolerance, liquidity needs, and expertise. It provides inflation protection, portfolio diversification, and current income that stocks and bonds don't offer. Focus on quality over quantity given current market uncertainty.

How can small investors access commercial real estate opportunities?

Small investors can access commercial real estate through REITs (public and private), real estate crowdfunding platforms, syndications with experienced sponsors, or direct ownership of smaller properties (small multifamily, retail, industrial). Each approach has different minimum investments, liquidity profiles, and fee structures.

Conclusion

Navigating the 2026 Capital Markets Fog: Strategies for Real Estate Investors Facing Economic Uncertainty demands discipline, patience, and a clear-eyed assessment of risks and opportunities. The elevated financing environment and ongoing price discovery have fundamentally changed the investment landscape, but opportunities exist for investors who adapt their strategies to current conditions.

The path forward requires several key actions:

Embrace conservative underwriting that stress-tests assumptions and doesn't rely on market improvement to generate returns. Use lower leverage, longer hold periods, and realistic growth projections that account for today's higher cost of capital.

Focus on cash flow and fundamentals rather than speculative appreciation. Properties must generate sufficient income to cover debt service with healthy margins while providing equity returns in the 12-15% range.

Prioritize core and core-plus assets in markets with diverse employment, population growth, and supply constraints. These defensive positions preserve capital during uncertainty while participating in upside when conditions improve.

Diversify across property types and markets to reduce concentration risk. Combine traditional sectors with alternatives that offer structural growth drivers, and spread investments across gateway and secondary markets.

Structure deals defensively with moderate leverage, fixed-rate long-term debt, adequate reserves, and flexible exit options. Protect downside while maintaining upside participation.

Monitor leading indicators including employment, absorption, and rent growth to make informed decisions about deployment timing and portfolio management.

Deploy capital patiently through a phased approach that allows you to take advantage of opportunities as they emerge rather than forcing capital into mediocre deals.

The investors who thrive in 2026's fog are those who accept the new market reality, underwrite conservatively, focus on quality assets with strong fundamentals, and maintain the financial flexibility to weather storms and capitalize on distress. The opportunities are there for those disciplined enough to find them and patient enough to wait for the right entry points.

Start by reviewing your current portfolio against the benchmarks outlined in this guide, identifying properties that may face refinancing challenges or operational headwinds. Build relationships with lenders, brokers, and operators in your target markets to access deal flow before it hits the broader market. And most importantly, maintain dry powder and discipline—the best opportunities in uncertain markets come to those prepared to act when others cannot.